by Sheraz Mian

May 31, 2013

The Q1 earnings season is effectively over and we still have a few more weeks to go before the next reporting cycle gets underway. The focus this week is on economic data, particularly the jobs report coming on Friday.

A handful of 2013 Q1 results are still awaited and quite a few of those will come out this week. Including Dollar General (DG – Snapshot Report), VeriFone (PAY – Analyst Report), J.M. Smucker (SJM – Analyst Report), Hovnanian Enterprises (HOV – Snapshot Report) and others, we will get Q1 results from 51 companies in total and 4 S&P 500 members. We are nearing the end point of Q1 earnings season and just a couple of weeks away from the point when the Q2 earnings season gets underway with reports from Discover Financial (DFS – Analyst Report) and Oracle (ORCL – Analyst Report) on June 17th.

Expectations for the 2013 Q2 earnings season have come down, with total earnings in the quarter now expected to be up +0.9% on -0.7% lower revenues. This is a drop from the +3.9% total earnings growth expected in Q2 on +0.5% higher revenues in early April. Total earnings were up +2.8% in Q1 on barely positive growth in revenues.

The Finance sector is expected to rebound strong in Q2, with total earnings for the sector expected to be up +19.1% from the same period last year after the +7.7% total earnings growth in Q1. The recent uptrend in long-term interest rates following the ‘Taper’ buzz has improved the operating backdrop for the sector quite a bit, with earnings estimates for the sector moving up. As you can see in the ‘revisions ratio’ charts below, the revisions trend is decidedly in the positive category for the sector.

Expectations for full-years 2013 and 2014 have come down far less than what we have seen for Q2 estimates. In fact, it is reasonable to assume that given the improving outlook for the Finance sector, aggregate estimates will start rising after a very long time in the coming weeks.

The +6% growth in total earnings this year, down from +6.8% in early April, reflects a material ramp up in the second half of the year that is then expected to carry into 2014. Combining the actual results for Q1 with estimates for Q2 gives us +1.8% year over year growth in total earnings in the first half of 2013. But total earnings are expected to be up +9.5% in the second half of the year and a further +11.5% in full-year 2014.

For a quick recap of the Q1 earnings season, please check this video . This Earnings Trends report provides a detailed look at the earnings picture.

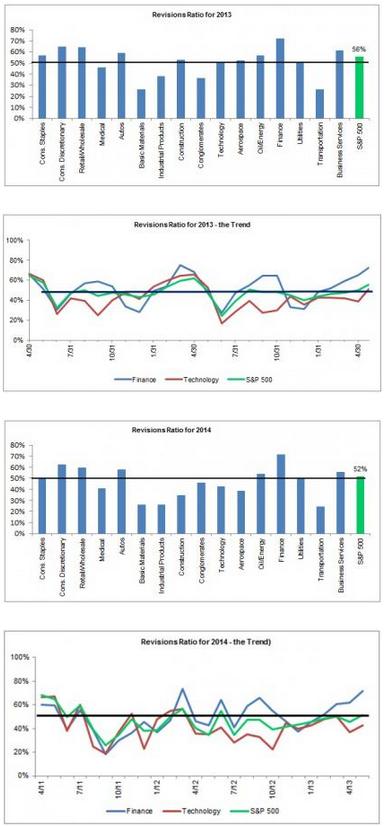

Trends in Estimate Revisions

The revisions trend has started moving in a positive direction, with more earnings estimates going up instead of down. Even accounting for the typical seasonal behavior of revisions activity which peaks during earnings seasons and tails off after the season is over or close to over, the emerging trend in revisions appears significant.

The charts below show trends in earnings estimate revisions. The key metric in all the charts is the ‘revisions ratio,’ which is the ratio of total number of upward revisions over the preceding four weeks to the total number of revisions (positive and negative) over that same period. We have two charts each 2013 and 2014. The bar charts show the current state of the ‘revisions ratio’ (as of 5/24/13), while the line charts plot the ratio’s trajectory over the preceding 24 months.

The ratio doesn’t tell you the ‘magnitude’ of the revisions, only the direction. The ‘50%’ level (the dark line) is the dividing line between positive and negative trends, with readings above 50% implying more positive than negative revisions. Our analysis shows that readings between 45% and 55% don’t offer material insights into the magnitude of revisions. It is only readings above 55% and below 45% that offer bullish and bearish signals about the magnitude of earnings revisions.

As you can see in the charts above, the revisions trend for the S&P 500 as a whole is still in neutral territory though moving in the right direction. But see the fast emerging positive trend in the Finance sector for both this year and next (the green line). The sector’s revisions ratio currently (as of 5/24) stands at 72%, by all means bullish territory. This pronounced positive bias is at play for many industry players that are experiencing positive estimate revisions, including J.P. Morgan (JPM – Analyst Report), Wells Fargo (WFC – Analyst Report), Fifth Third Bank (FITB – Analyst Report) and many others.

The trend makes perfect sense as higher interest rates may be a hindrance for other industries, but it’s beneficial for the Finance sector’s earnings. Flat net-interest margins have been a permanent feature of the sector’s — particularly banking’s — earnings picture in recent quarters. The charts also show the trend in the Technology sector, the largest in the S&P 500, to spotlight Finance’s improving outlook.

The Finance sector’s positive earnings outlook is a function of the rising trend in interest rates. But whether that trend continues or reverses course in the coming days will depend to a large extent on economic data this week, particularly Friday’s May non-farm jobs report. A positive jobs report on Friday will significantly increase the odds of a ‘Taper’ announcement in the coming FOMC meeting.

The market’s anticipation of the Fed’s plans to taper its monthly bond purchases has been the primary driver pushing bonds yields higher. There is plenty of other economic data coming out this week as well, including the two ISM surveys, motor vehicle sales numbers, Construction Spending and the Fed’s Beige Book.

Monday – 6/3

The May Manufacturing ISM survey will be the key report today, though we will also be getting the April Construction Spending and the May motor vehicle sales numbers.

The expectation is for the ISM reading to come in at 51.7 after the 50.7 reading in April, but the strong showing by the Chicago PMI improves the odds of a positive surprise here. A strong ISM reading will be interpreted as a net negative by the market given its recent ‘Taper’ fixation.

ABM Industries (ABM), Cracker Barrel (CBRL) and SAIC (SAI) are the only notable reports today.

Tuesday – 6/4

The April Trade Deficit is the only economic report on the docket, with expectations of an increase from March’s $38.8 billion deficit level.

Dollar General (DG – Snapshot Report) and American Woodmark (AMWD) are the key earnings reports today, both in the morning.

Wednesday – 6/5

A very busy day on the economic calendar, with the May ADP jobs report and Q1 productivity readings coming out before the market’s open. Also coming out today are the Non-manufacturing ISM report for May, the April Factory Orders report, and the Fed’s Beige Book.

The consensus expectation is for the ADP report to show 183K private sector jobs, up from April’s 119K level. A strong ADP report will set market expectations for the Friday jobs report from the government’s Bureau of Labor Statistics (BLS).

Brown Forman (BF.B), Hovnanian Enterprises (HOV – Snapshot Report) are the only notable earnings reports in the morning, while VeriFone (PAY – Analyst Report) will report after the close.

Thursday – 6/6

The weekly Jobless Claims numbers coming out this morning are expected to show a reversal of the prior week’s jump in initial claims.

J.M. Smucker (SJM – Analyst Report) and Titan Machinery (TITN) are the key reports in the morning, while Cooper Companies (COO) will report after the close.

Friday – 6/7

The May non-farm payroll report from the government’s BLS is the day’s highlight and will set the tone for the stock market not just for today, but also for the coming days. The expectation is for a ‘headline’ tally of 175K jobs after April’s 165K tally. A strong jobs report will be a negative for the market.

Filed under: Investing, Uncategorized | Tagged: Discover, Dollar General, Fifth Third, finance, Hovnanian, Investing, investments, JP Morgan, money, Oracle, Smuckers, stock market, VeriFone, Wells Fargo | Leave a comment »